Two Key Points to Consider in Determining Whether to Buy Your Home Now or Later

Home Prices & Mortgage Rates

No joke you say. I know; I state the obvious here. However, if you are one of the many folks contemplating purchasing a home, you are likely trying to hedge your bets on the right timing to act. You want to hit a jackpot of lower housing prices paired with lower interest rates. You may be getting your real estate market information from a wide range of places such as the nightly news to Aunt Annie’s opinions, for you to formulate your conclusion on when to strike. Allow me to help you out.

Home Prices

Let’s clear up the market chatter you've heard and look at the chart by CoreLogic below. This data comes from a study of home prices nationwide and forecasts a 1% increase of home prices from May 2023 to June 2023 and forecasts an increase of 4.5% from May 2023 to May 2024.

CoreLogic Home Price Index (HPI) Forecast Chart

“After peaking in the spring of 2022, annual home price deceleration continued in May. Despite slowing year-over-year price growth, the recent momentum in monthly price gains continues.” Selma Hepp, Chief Economist for CoreLogic

If you are anticipating a housing crash, don’t hold your breath, the price “deceleration” phase appears to be short lived. In fact, based on this forecast, the prices will continue to increase, but fortunately not at the same pace as they have been. Plus, we are still contending with a nationwide housing shortage which directly impacts prices. Ah yes, the supply (where are the houses??) and the demand (we all want one!!) principle is real. The point being, if you buy now, you will begin building equity with your home’s appreciation. If you wait to buy later, the house will cost you more money.

What about the mortgage rates though?

As you well know, mortgage rates climbed significantly this past year. Why? Because our nation has been dealing with high inflation and to combat it, the Feds steadily raised the rates to slow down the economy. Now that we are past the peak of 9% inflation from June 2022, with June 2023’s number at 3%, we expect to see some good news for borrowers. Because when inflation cools, mortgage rates tend to as well.

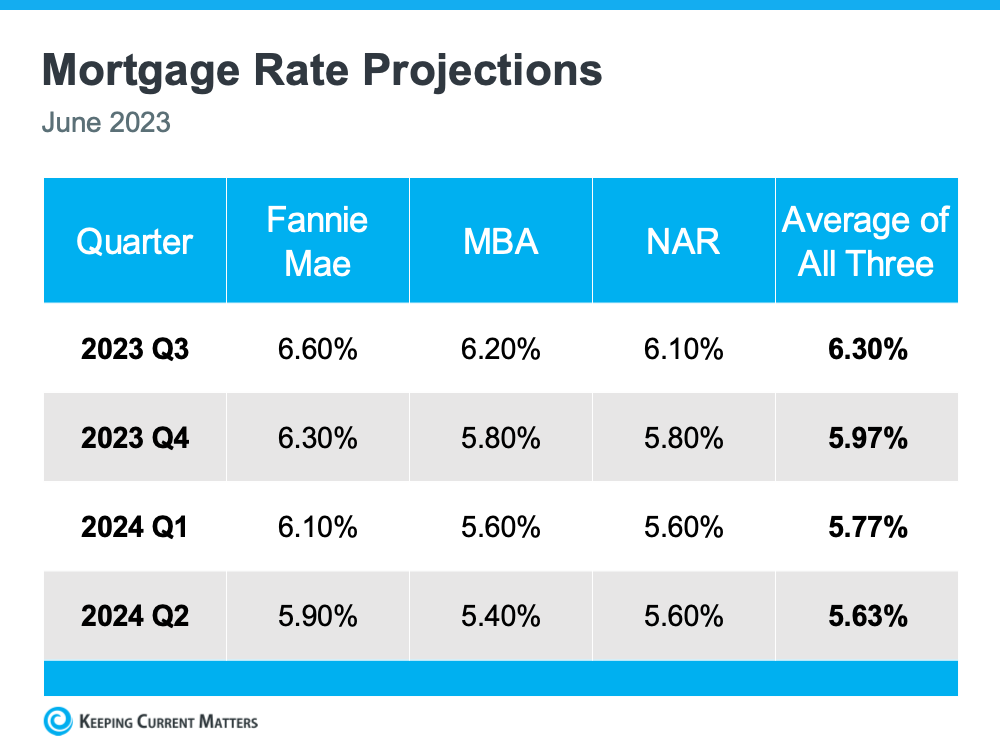

Check out this chart:

To be clear, these highly informed expert opinions above aren’t etched in stone projections, because there are many factors that impact mortgage rates. Nonetheless, we are projected to see some relief. Yay!

Scenarios to contemplate if you decide to buy now:

- If you purchase now, and the rates remain the same, you’re in good shape because homes are projected to continue to appreciate (hello equity), and you got in ahead of the rising prices.

- If you buy now and the rates drop, you are still in good shape because you bought your house before it became more expensive, you’re earning equity and you can refinance later when the rates decrease.

- If you buy now and the rates go up, well then, awesome for you. You got in before the cost of the house and the rate of the mortgage increased.

So, yeah, looking at it from different angles, buying now is beneficial.

Knowledge is power when you are considering buying a home. There is no perfect crystal ball we can peer into for guaranteed projections, but the experts provide incredibly knowledgeable insight with their forecasting. I have been sharing market data based on our country as a whole. Contact me if you would like an opinion focused on your local market. Because there can be a difference from looking at the nation as a whole and drilling down to your hometown.

By Karen Alsheimer®

Question Mark Photo courtesy of: Free Stock photos by Vecteezy